The Duty Drawback Blog

Our blog articles are written by our team of experts with the knowledge and experience to identify and implement cost-saving strategies for your business. Let us guide you through the Duty Drawback process and ensure that you're taking advantage of all available opportunities. We endeavor to provide actionable advice that can help you optimize your supply chain and boost your bottom line.

For nearly eight years, Section 301 tariffs have been one of the most significant trade measures affecting U.S. importers. While many tariff programs have been challenged in court, modified, or even struck down, the Section 301 tariffs on Chinese goods have survived extensive legal scrutiny and remain a key component of U.S. trade policy.

Section 301 tariffs are confirmed permanent after SCOTUS declines appeal. CAPE Phase 2 opens $28.7B in refunds. ITM explains what importers need to do now.

CBP is intensifying customs enforcement under Trump's new EO. Review your HTS classification and valuation practices before auditors do. ITM can help.

DOJ appeals IEEPA refund order, putting $166B at risk for non-plaintiff importers. Section 122 struck down but expires July 24. June 2026 update from ITM.

CAPE is live — IEEPA refund claims are open. CBP goes ACH-only for all drawback payments. Audits are surging. ITM's May 2026 trade compliance update.

$165B in IEEPA tariff refunds ordered by court. New Section 301 investigation opens. CBP limits AI customs platforms. ITM's April 2026 trade compliance update.

IEEPA tariffs ruled illegal by the Supreme Court — CBP has stopped collecting. New Section 122 duties are now in effect. Here's what importers need to know.

JTV cut duty drawback workload 50% after switching to ITM. See how Jewelry Television recovered a near-complete backlog and transformed their entire process.

Ed Greenberg, Managing Director of PEM America, explains the hundreds of thousands of dollars his company recovered through duty drawback.

Supreme Court will soon rule on IEEPA tariffs. Learn the 3 steps importers must take now to protect refund rights before liquidation deadlines pass.

$450K in duty refunds realized through a detailed analysis and evaluation of duty-free classifications made by International Tariff Management.

January 2026 trade update: OBBBA targets tobacco drawback, Section 232 delayed, reciprocal tariffs still eligible for refunds. Plus: why 2026 is enforcement year.

2025 began with the promise and the introduction of sweeping, high tariffs on nearly all imports. While there was a transition to a two-tiered system including broad tariffs and country-specific rates, the mid-year brought pauses, renegotiations, and recalibrations.

The benefits that we realized working with International Tariff Management was that they made the process seamless from beginning to end.

Oral arguments are scheduled to begin this week with the Supreme Court in regards to the Reciprocal Tariffs - starting Wednesday November 5, 2025.

The Supreme Court, which resumed on October 6th, has agreed to hear the case in regards to the reciprocal-tariffs (IEEPA), on an expedited basis.

By leveraging the option to claim drawback on items launched into space, the importer was able to recover substantial funds — and cover these unexpected costs which they in turn did not have to pass along to their manufacturing partners.

The latest on the reciprocal tariffs have them hanging in the balance. On August 29, 2025, the U.S. Court of Appeals for the Federal Circuit, affirmed a lower court decision finding that the reciprocal tariffs exceeded presidential authority under IEEPA. The court stayed its mandate until October 14, 2025, giving the g

The Department of Justice (DOJ) has officially elevated trade and customs fraud—including tariff evasion—to its #2 enforcement priority. This shift is part of a broader strategy under the Trump administration to enforce high tariffs and ensure accurate revenue collection.

On July 27th, the Trump Administration announced a deal with the EU imposing tariffs of 15% on most goods entering the US from Europe. As of August 1st, the 15% blanket tariff will cover most US imports. The US will have a 0% tariff for some items including equipment for US manufacturing and generic medicines.

Last week, it was announced that the U.S. had reached a preliminary trade agreement with Vietnam. The agreement involves a 20% tariff on Vietnamese goods.

The American company reached out to ITM for guidance. They were pleased to learn that under U.S. Customs regulations, they could file for duty drawback—a refund of duties paid—on expired and destroyed goods. Within just four months, ITM had successfully obtained the required authorizations and filed all claims related to the product destructions. Due to ITM’s relationship USCBP, and their expertise, over $850,000 in duty refunds was recouped.

On May 28, 2025, a U.S. trade court ruled that President Donald Trump over stepped his authority in imposing the reciprocal tariffs. At that time, the court ordered an immediate block on said tariffs. As of May 29, 2025 a federal appeals court temporarily reinstated the most sweeping of Trump's tariffs. Pausing the lower court’s ruling, The United States Court of Appeals for the Federal Circuit in Washington is going to consider the government's appeal, and has ordered the plaintiffs in the cases to respond by June 5 and the administration by June 9. This is a developing situation and we will do our best to keep the information coming.

This jewelry retailer's duty drawback success story demonstrates the significant impact that a well-managed duty drawback program can have on profitability. By recovering significant funds, the jewelry retailer was able to reinvest in their business, enhance competitiveness, and strengthen their bottom line in a challenging market.

Effective at 12:01 a.m. on April 5, 2025, a 10% baseline tariff on imported goods from most countries, with a few exceptions, will be implemented. This baseline is in addition to regular duties and fees, current IEPPA duties, Section 201 duties, Section 301 duties, and any applicable AD/CVD.

As of 12:01am, March 4, 2025, tariffs of 25% are effective on products from Canada and Mexico and energy products from Canada are subject to a 10% duty. Products that are presently excluded from these tariffs include goods that are for personal use, goods entered under Chapter 98, donations that are imported under HTSUS 9903.01.21and merely information items included under HTSUS 9903.01.22. All other imported items will carry the 25% tariff and no drawback is permitted on these duties.

The upcoming changes to steel and aluminum tariffs will significantly impact the steel and aluminum industries, with numerous provisions to ensure compliance. Importers, exporters, and manufacturers in the steel and aluminum sectors should stay informed about the latest developments and ensure their operations are aligned with these new tariff regulations.

On February 1, 2025, President Trump signed an Executive Order (EO) that imposes an additional 10% ad valorem tariff on most imports from China, which includes products of Hong Kong. U.S. Customs and Border Protection (CBP) quickly followed up with important guidance regarding these changes, particularly impacting the trade community's handling of de minimis shipments from China. Effective February 4, 2025, de minimis shipments from China will no longer be eligible for the administrative exemption from duty under 19 U.S.C. § 1321(a)(2)(C), and will be subject to the new 10% tariffs. Here's everything you need to know about the changes:

The recent guidance from U.S. Customs and Border Protection (CBP) regarding de minimis shipments from China is a significant update. The EO signed by President Trump on February 1, 2025, imposed an additional 10% tariff on U.S. imports from China.

On January 20, 2025, President Donald Trump was sworn in for his second term, and with that came big promises regarding trade policy. But a significant shift came just days later, on January 21, when Trump announced plans to impose 25% tariffs on Mexico and Canada—set to go into effect on February 1, 2025.

On January 20, 2025, President Donald Trump was sworn in for his second term, and with that came big promises regarding trade policy. But a significant shift came just days later, on January 21, when Trump announced plans to impose 25% tariffs on Mexico and Canada—set to go into effect on February 1, 2025. This move represents a dramatic change in North American trade relations and could have wide-reaching effects on American consumers. At a signing ceremony in the Oval Office, Trump revealed that his administration would roll out tariffs on goods from two of the U.S.'s largest trading partners, Mexico and Canada. However, this new tariff decision doesn’t fully align with the aggressive trade strategy Trump promised during his campaign. The sweeping tariffs Trump pledged on his first day in office, including a 25% tariff on Mexico and Canada, have yet to materialize. His executive action, while still outlining a broad trade policy overhaul, serves more as a placeholder for a more extensive, long-term plan.

Although the United States and Taiwan (officially known as the Republic of China) do not maintain formal diplomatic relations, the two countries share strong cooperation in several areas, including trade. Trade discussions are managed through the American Institute in Taiwan and the Taipei Economic and Cultural Representative Office in the U.S., under an arrangement called the U.S.-Taiwan Initiative on 21st Century Trade. This framework allows both nations to address trade and investment issues, while working toward mutual priorities over time.

As of January 1, 2025, new tariff rates on certain Chinese imports will go into effect, as part of the ongoing Section 301 investigation into China's trade practices, particularly regarding technology transfer, intellectual property, and innovation. The United States Trade Representative (USTR) has announced additional tariff increases under the Section 301 Four Year Review, which impacts a range of products, including certain tungsten products, solar wafers, and polysilicon. If you're involved in importing these products or handling customs filings, it’s crucial to understand the latest developments and the steps required to comply with the updated regulations.

Our team is excited to be back for another year of maximizing refunds and providing exceptional service for our partners!

In his recent article, "Why China Welcomes Trump’s Energy Tariffs", energy and geo-economics expert Wesley Alexander Hill provides an intriguing take on how U.S. tariffs, especially those targeting energy products, might inadvertently benefit China rather than harm it, as intended by former President Donald Trump.

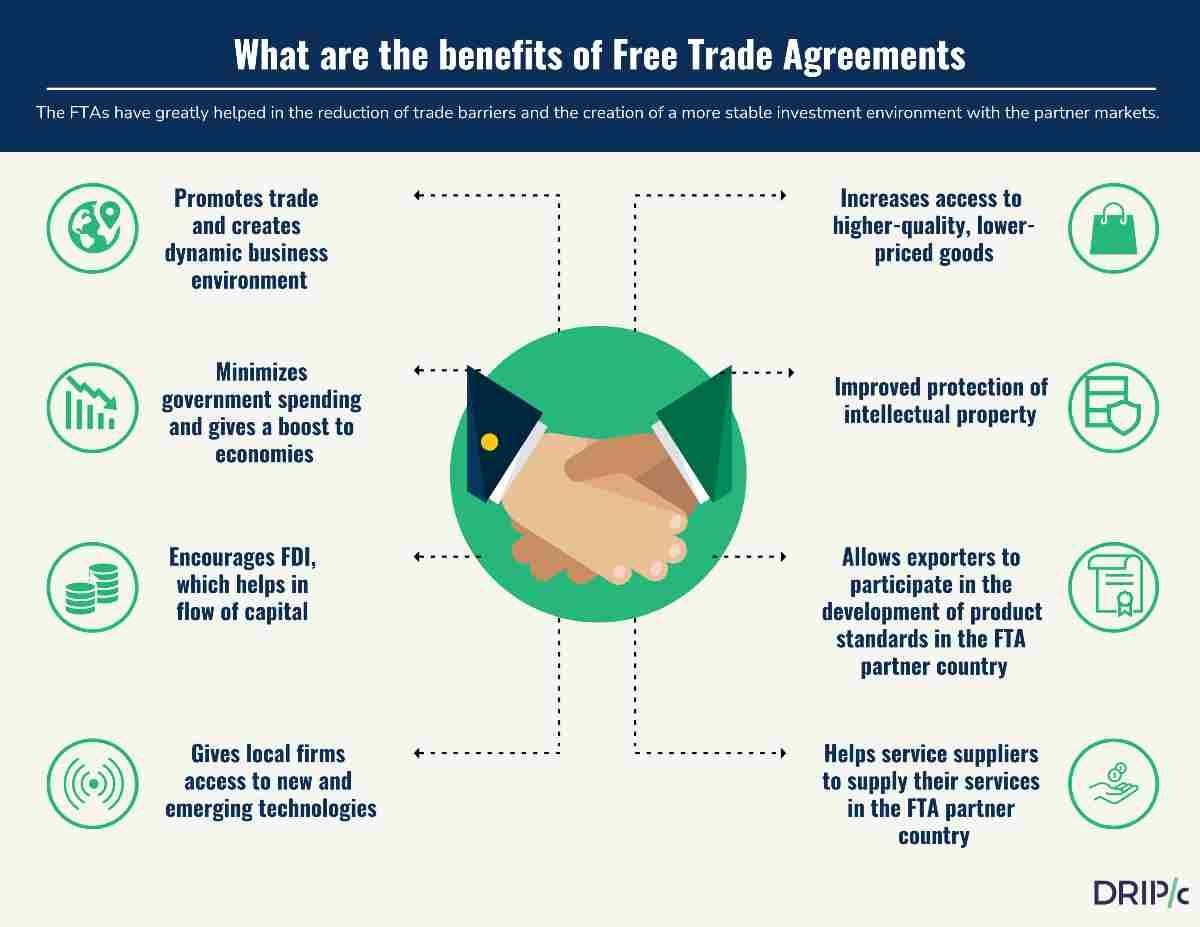

Dr. Naushad Forbes explains the issues surrounding around the WTO and the benefits of utilizing Free Trade Agreements

Free Trade Agreements (FTAs) and U.S. Economic Influence: A Snapshot of 20 Countries Free trade agreements (FTAs) are vital tools for the United States, designed to open international markets to American businesses, enhance the competitiveness of U.S. products abroad, and give consumers access to a broader range of goods in the global marketplace. These agreements also grant the U.S. increased political influence, integrating partner countries into the American economy and making them less likely to align with rivals such as China or Russia. Republican presidents have typically championed FTAs, viewing them as beneficial to business and an essential means of exerting American influence internationally. However, FTAs are controversial. Critics argue that they can lead to the relocation of jobs overseas, as businesses seek to produce goods where labor and materials are cheaper. There are also concerns that FTAs can erode local cultures and lead to cultural homogenization, which is often felt more acutely by smaller, less dominant cultures. These concerns have made FTAs less popular within the Democratic Party.

On December 11, 2024 , the U.S. Trade Representative (USTR) announced increases in tariffs on certain tungsten products, wafers, and polysilicon, following its September 19, 2024, solicitation for comments. These tariff increases will take effect for goods entered on or after January 1, 2025 , and are part of the USTR’s final action under the statutory four-year review of existing Section 301 duties on China.

Happy Holidays! Our team wishes everyone the best in the coming year.

With Donald Trump returning to the presidency, global trade professionals are facing an uncertain and rapidly evolving landscape. Given his past policies and rhetoric, significant shifts in the global trade environment seem likely—shifts that could have far-reaching effects on international markets and economies. In this post, we’ll explore the potential implications of a second Trump presidency on global trade, the key role of trade professionals in adapting to these changes, and crucial areas of focus such as the De Minimis rule, Most-Favored-Nation (MFN) status, export controls, and investment restrictions.

As the possibility of renewed Trump-era tariffs looms, industries are already planning how to protect their supply chains from potential disruptions. President-Elect Donald Trump has proposed imposing blanket tariffs of up to 20% on all imports, and even higher tariffs—ranging from 60% to 100%—on goods from China.

Updates in FTA's and GSP with significant effects of the state of trade for the United States.

For over three decades, the European Union (EU) and the Gulf Cooperation Council (GCC) have been trying to finalize a free trade agreement (FTA). However, despite early talks, the deal has remained elusive. The main roadblock? The EU's tendency to mix economic issues with political and ideological concerns—an approach that has ultimately hindered progress.

The US-Morocco Free Trade Agreement (MAFTA), signed in 2004 under President George W. Bush, was a landmark deal aimed at strengthening economic and strategic ties between the U.S. and Morocco.

In a significant development for U.S.-Chile trade relations, the two nations have approved a pivotal agreement that bolsters the existing Free Trade Agreement (FTA) between them. This new accord, formalized through an exchange of letters, introduces enhanced protections for U.S. cheese exports to Chile—an essential market for American dairy products.

The lapse of the GSP has not only disrupted these economic plans but has also intensified the geopolitical landscape. As the U.S. grapples with domestic political divisions and a rethinking of its trade policies, China has stepped into the breach.

U.S. Customs and Border Protection (CBP) has recently issued a crucial reminder to businesses regarding the compliance requirements for drawback claims. As many companies navigate the complexities of customs regulations, it’s essential to understand the consequences of failing to meet these requirements.

The U.S. Trade Representative's Office released their four-year review of the Section 301 Tariffs which call for retaining the duties currently in place along with an increase on entire classes of Chinese imports.

CBP made an update to the Automated Commercial Environment or ACE Portal which will be useful to brokers and filers. Import refunds are now visible through the Broker’s ACE Portal Account. Using the REV - 603 report, you can now search for refunds by utilizing refund date search parameters.

In the intricate world of international trade, various mechanisms exist to facilitate smoother transactions and encourage commerce across borders. One such mechanism is duty drawback, a process that offers significant benefits to businesses engaged in importing and exporting goods. In this guide, we will delve into the concept of duty drawback, its benefits, and how businesses can leverage it to their advantage.